Sold a stock, flipped a property, or cashed out crypto before the one-year mark? The IRS treats those profits differently than gains you waited to take, and the difference in taxes owed can be significant.

This guide breaks down every 2026 short-term capital gains tax rate, bracket, and rule, including real estate, married filing jointly thresholds, and the strategies that actually reduce your bill.

What is Short-Term Capital Gains Tax?

A capital gain is simply the profit you make when you sell something for more than you paid for it. The IRS splits these gains into two categories based on how long you owned the asset before selling:

- Short-term: You held the asset for 365 days or fewer. The IRS taxes the profit at your ordinary income rate.

- Long-term: You held the asset for more than one year. You qualify for preferential rates of 0%, 15%, or 20%.

That distinction matters enormously. The same $50,000 gain on a stock could cost you $18,500 in federal tax at the 37% rate if you sell too soon, or as little as $7,500 at the 15% long-term rate if you waited a year.

One important detail on the holding period: The clock starts the day after you buy the asset and ends on the day you sell. Buy a stock on January 15, 2026, and sell it on January 15, 2027, that is exactly 365 days and still counts as short-term. Sell on January 16, 2027, and it becomes a long-term gain. One day can change the outcome.

What Counts as a Short-Term Capital Gain?

Profits from selling stocks, bonds, ETFs, mutual funds, cryptocurrency, real estate, collectibles, or any other capital asset held for one year or less. Your broker reports these on Form 1099-B, and you report them on Schedule D of your tax return using Form 8949.

2026 Short-Term Capital Gains Tax Rates and Brackets

Short-term gains are taxed at your ordinary income tax rate. The IRS released its 2026 inflation-adjusted brackets under Rev. Proc. 2025-32, reflecting roughly 2 to 3% increases across most thresholds. Here are the 2026 rates for every filing status:

Single Filers

| Tax Rate | Taxable Income (2026) | Tax Owed |

|---|---|---|

| 10% | Up to $11,925 | 10% of taxable income |

| 12% | $11,926 to $48,475 | $1,192.50 + 12% over $11,925 |

| 22% | $48,476 to $103,350 | $5,578.50 + 22% over $48,475 |

| 24% | $103,351 to $197,300 | $17,651.50 + 24% over $103,350 |

| 32% | $197,301 to $250,525 | $40,199.50 + 32% over $197,300 |

| 35% | $250,526 to $626,350 | $57,231.50 + 35% over $250,525 |

| 37% | Over $626,350 | $188,769.75 + 37% over $626,350 |

Source: IRS Rev. Proc. 2025-32 · 2026 Tax Year (returns filed in 2027)

Married Filing Jointly (MFJ)

| Tax Rate | Taxable Income (2026) |

|---|---|

| 10% | Up to $24,800 |

| 12% | $24,801 to $100,800 |

| 22% | $100,801 to $211,400 |

| 24% | $211,401 to $403,550 |

| 32% | $403,551 to $512,450 |

| 35% | $512,451 to $768,700 |

| 37% | Over $768,700 |

Source: IRS Rev. Proc. 2025-32 · 2026 Tax Year

Head of Household

| Tax Rate | Taxable Income (2026) |

|---|---|

| 10% | Up to $17,700 |

| 12% | $17,701 to $67,450 |

| 22% | $67,451 to $105,700 |

| 24% | $105,701 to $201,750 |

| 32% | $201,751 to $256,200 |

| 35% | $256,201 to $640,600 |

| 37% | Over $640,600 |

Married Filing Separately

| Tax Rate | Taxable Income (2026) |

|---|---|

| 10% | Up to $12,400 |

| 12% | $12,401 to $50,400 |

| 22% | $50,401 to $105,700 |

| 24% | $105,701 to $201,775 |

| 32% | $201,776 to $256,225 |

| 35% | $256,226 to $384,350 |

| 37% | Over $384,350 |

Important: These Are Marginal Rates

Only the income within each bracket gets taxed at that rate, not your entire gain. A short-term gain that pushes you into the 32% bracket does not mean all of your income is taxed at 32%. Just the portion above the bracket threshold gets hit at the higher rate.

Short-Term vs. Long-Term Capital Gains: Side-by-Side Comparison

| Factor | Short-Term (2026) | Long-Term (2026) |

|---|---|---|

| Holding period | 365 days or fewer | More than 365 days |

| Federal tax rate | 10% to 37% | 0%, 15%, or 20% |

| Basis for rates | Ordinary income brackets | Separate capital gains brackets |

| NIIT applies? | Yes (if income exceeds threshold) | Yes (if income exceeds threshold) |

| State taxes? | Yes, most states tax the same as income | Some states offer preferential rates |

| Best for? | Unavoidable or loss-generating situations | Most buy-and-hold investors |

Real-World Example

Sarah is a single filer with $120,000 in wages. She also sold stock for a $40,000 profit after holding it for 8 months.

Her total taxable income is $160,000. The $40,000 short-term gain is taxed at ordinary income rates, and the portion falling in the 24% bracket gets taxed at 24%.

Federal tax on the gain: approximately $9,600.

Had she waited four more months to sell, that same $40,000 would qualify as a long-term gain. At her income level, the long-term rate would be 15%, cutting the tax bill to $6,000. Waiting cost her nothing. Selling early cost her $3,600.

Short-Term Capital Gains Tax on Real Estate

There is no special real estate short-term capital gains rate. If you sell a home, rental property, or land you owned for one year or less, the profit is taxed as ordinary income, just like selling a stock.

That means a real estate investor in the 32% bracket could owe nearly a third of their profit on a quick flip. Add state income tax and the NIIT, and the real cost can climb past 40%.

The Primary Residence Exclusion

There is one major exception. If you are selling your primary home and have lived there for at least two of the past five years, the IRS lets you exclude up to $250,000 of gain ($500,000 if married filing jointly) from your taxable income. This exclusion applies regardless of short- or long-term status.

The catch: this only applies to your main residence. Vacation homes, investment properties, and flips do not qualify for the exclusion. Those gains are fully taxable at your ordinary income rate if held for less than a year.

Capital Gains Tax on a House Sale: Quick Example

| Scenario | Gain | Holding Period | Tax Treatment |

|---|---|---|---|

| Primary home (lived in 2+ years) | $200,000 | 3 years | $0 (exclusion applies) |

| Rental property flip | $80,000 | 9 months | Ordinary income rate (up to 37%) |

| Investment property | $120,000 | 18 months | Long-term rate (0%, 15%, or 20%) |

Hidden Surcharges: NIIT and IRMAA

This is where many investors get surprised. The bracket tables show rates up to 37%, but two additional charges can quietly push your real rate much higher.

Net Investment Income Tax (NIIT): +3.8%

The NIIT adds a flat 3.8% tax on top of ordinary rates for investors whose Modified Adjusted Gross Income (MAGI) exceeds:

- ►$250,000 for married filing jointly

- ►$200,000 for single filers

- ►$125,000 for married filing separately

The NIIT threshold has not been adjusted for inflation since the tax was created in 2013. Every year, more households get caught by it without realizing it applies to them.

IRMAA Medicare Surcharges

Short-term gains raise your MAGI, which Medicare uses to set your premium amounts, with a two-year lookback. If a large gain pushes your MAGI above certain thresholds, you could face hundreds or even thousands in extra Medicare premium costs that show up two years after the transaction.

“A $200,000 short-term gain in a high-tax state could cost 54 to 56% of the profit when you add federal rates, NIIT, and state income tax together.”

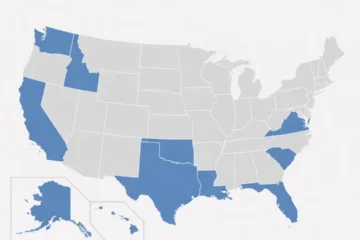

State Taxes on Short-Term Capital Gains

Most states tax short-term capital gains as ordinary income, meaning you owe both federal and state tax on the same profit. State rates vary widely:

| State | Top Rate on Short-Term Gains | Notes |

|---|---|---|

| California | 13.3% | Highest in the U.S.; no preferential rate |

| New York | 10.9% | Plus NYC tax of up to 3.876% |

| New Jersey | 10.75% | Treated as ordinary income |

| Oregon | 9.9% | No special capital gains treatment |

| Texas | 0% | No state income tax |

| Florida | 0% | No state income tax |

| Nevada | 0% | No state income tax |

| Washington | 7%* | *On long-term gains over $250,000 only |

Living in a no-income-tax state like Texas or Florida means you only owe federal short-term capital gains tax. That can represent a meaningful difference, especially for high-income earners or investors with large gains.

2026 Long-Term Capital Gains Tax Brackets (For Comparison)

Understanding the short-term rates is more useful when you see them side by side with the long-term rates you are trying to qualify for.

Long-Term Capital Gains Rates: All Filing Statuses (2026)

| Rate | Individuals (Single) | Married Filing Jointly | Head of Household | Married Filing Separately |

|---|---|---|---|---|

| 0% | $0 to $49,450 | $0 to $98,900 | $0 to $66,200 | $0 to $49,450 |

| 15% | $49,451 to $545,500 | $98,901 to $613,700 | $66,201 to $579,600 | $49,451 to $306,850 |

| 20% | $545,500+ | $613,700+ | $579,600+ | $306,850+ |

A married couple with $150,000 in taxable income who takes a $50,000 capital gain after holding for one year pays 15% federal tax on that gain, which is $7,500. If they sold just two months earlier and triggered a short-term gain, the same profit could be taxed at 22 to 24%, costing $11,000 to $12,000. The year-and-a-day rule is one of the most financially significant waiting periods in tax law.

How to Reduce Short-Term Capital Gains Tax in 2026

You cannot always control the timing of a sale, but when you can, these strategies meaningfully lower the short-term capital gains tax you owe:

- Wait for Long-Term Status: The simplest and most powerful move: hold the asset for more than 365 days before selling. The tax savings alone can represent a 15 to 17 percentage point drop in your rate on that gain.

- Tax-Loss Harvesting: Offset your short-term gains by selling other investments that have lost value. The IRS lets you use capital losses to offset capital gains dollar for dollar. Losses that exceed gains can reduce your ordinary income by up to $3,000 per year, and the rest carries forward.

- Use Tax-Advantaged Accounts: Gains inside a 401(k), IRA, HSA, or 529 plan are not subject to capital gains tax while the money stays in the account. If you plan to actively trade or invest in higher-turnover strategies, doing it inside a tax-deferred or tax-free account removes the short-term gain problem entirely.

- Spread the Gain Across Years: If you are selling a business, real estate, or another large asset, an installment sale lets you receive payment and recognize the taxable gain across multiple tax years. This can keep you in lower brackets each year rather than taking a single large hit.

- Time Your Sale Around Lower-Income Years: If you know your income will be significantly lower next year, such as a gap year, early retirement, or a business downturn, waiting to sell can drop you into a much lower bracket, reducing the rate applied to the same gain.

- Donate Appreciated Assets: Donating appreciated property to a qualified charity allows you to deduct the fair market value and avoid capital gains entirely. This works especially well for assets with large embedded gains where a sale would trigger a significant short-term tax bill.

Short-Term Capital Gains Tax on Crypto in 2026

Cryptocurrency is treated as property by the IRS, not currency. That means all the same capital gains rules apply, including the short-term/long-term distinction.

Sell Bitcoin, Ethereum, or any other digital asset after holding it for less than a year, and the profit is taxed as a short-term capital gain at ordinary income rates.

The big change in 2026: Starting January 1, 2026, brokers are required to report digital asset transactions to the IRS on Form 1099-DA. This means crypto gains are now tracked and reported to the IRS in the same way stock transactions have been for years. The days of crypto gains going unreported are functionally over.

Also Taxable as Short-Term Gains

Using crypto to purchase goods or services, exchanging one cryptocurrency for another, and receiving crypto as payment for services all count as taxable events and may generate short-term capital gains depending on your holding period and cost basis.

What Changed for 2026: New AMT Rules

The One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, made the current tax bracket structure permanent, eliminating the uncertainty that had surrounded the 2017 Tax Cuts and Jobs Act’s scheduled expiration.

One significant change affecting investors with large short-term gains: the Alternative Minimum Tax (AMT) phase-out threshold was lowered from $1,252,700 to $1,000,000 for married couples filing jointly. Investors with substantial short-term gains now have a wider exposure window for AMT calculations, which can create unexpected additional tax liability.

The 2026 standard deductions also increased modestly:

- ►Single filers: $16,100 (up from $15,750 in 2025)

- ►Married filing jointly: $32,200 (up from $30,000 in 2025)

- ►Head of household: $24,300

A higher standard deduction lowers your taxable income, which can reduce the effective rate applied to a short-term gain, but only if you do not itemize.

Frequently Asked Questions

Q. What is the short-term capital gains tax rate for 2026?

Short-term capital gains are taxed at your ordinary income tax rate, which ranges from 10% to 37% depending on your total taxable income and filing status. There is no flat short-term capital gains rate. The rate depends on your full income picture.

Q. How long do I need to hold an asset to avoid short-term capital gains tax?

You need to hold the asset for more than 365 days (one year plus at least one day) to qualify for long-term capital gains rates. The holding period starts the day after you acquire the asset and ends on the day you sell it.

Q. Is there a short-term capital gains tax calculator for 2026?

Yes. Several tools are available at sites like SmartAsset.com and NerdWallet.com. To estimate on your own, find your projected taxable income including the gain, identify your marginal bracket from the tables above, and apply that rate to the gain amount that falls within each bracket.

Q. Do I owe short-term capital gains tax on real estate?

Yes. If you sell a property you owned for one year or less, the profit is taxed as ordinary income at your regular tax rate. The only major exception is the primary residence exclusion, which can shield up to $250,000 (single) or $500,000 (married) in gains if you have lived in the home for at least two of the past five years.

Q. What is the short-term capital gains tax rate in California for 2026?

California taxes short-term capital gains as ordinary income at the state level, with a top marginal rate of 13.3%. Combined with the federal rate of up to 37% and the 3.8% NIIT, high-income California residents can face a combined marginal rate of over 54% on short-term gains.

Q. Can I offset short-term capital gains with capital losses?

Yes. The IRS requires you to first net short-term gains against short-term losses, and long-term gains against long-term losses. If you have more losses than gains in one category, the excess can offset gains in the other category. Any remaining net capital loss can reduce ordinary income by up to $3,000 per year, with the rest carrying forward to future tax years.

Q. Are short-term capital gains tax brackets for married filing jointly different from single?

Yes. The married filing jointly (MFJ) thresholds are approximately double the single filer thresholds at most brackets, which can significantly reduce the effective rate on the same amount of income. For example, a $200,000 short-term gain puts a single filer solidly in the 32% bracket, while a joint filer with the same total income stays in the 24% bracket.

The Bottom Line

Short-term capital gains tax is one of the most avoidable taxes in the federal code, but only if you understand the rules. The rates are the same as ordinary income, they stack on top of your other earnings, and they can trigger hidden surcharges like the NIIT that most people do not see coming.

The most effective thing you can do in most situations is simply wait. One extra day of holding can shift a gain from short-term to long-term, lowering your rate by 15 percentage points or more on the same profit. When waiting is not an option, tax-loss harvesting, tax-advantaged accounts, and proper timing around your income picture can all meaningfully reduce what you owe.

If your gains are substantial, especially in a high-tax state like California or New York, talking to a CPA before you sell can save you far more than the cost of the advice.